[ad_1]

By Anto Antony

In late April, Indian officials in plainclothes raided the Bengaluru offices of Byju’s, seizing laptops and publicly linking the world’s most valuable education-technology startup with possible foreign exchange violations.

An ocean away, Byju Raveendran, the firm’s eponymous founder and chief executive, paced his condo in Dubai, downing cups of black coffee and fielding calls from top investors. With a planned $1 billion equity fundraise from Middle Eastern investors still in limbo, Raveendran broke down in tears defending his company, according to people who attended the calls.

Raveendran had been in crisis mode for months. Apart from the raid by India’s financial crime-fighting agency, his once high-flying tutoring startup failed to file its financial accounts on time. Several US-based investors accused Byju’s of hiding half a billion dollars, prompting lawsuits.

On Tuesday, Prosus NV, one of the company’s earliest investors, said it had given up its board seat because of poor governance and disregard for directors’ advice.

Byju’s and Raveendran have denied wrongdoing. But their tale — pieced together from interviews with more than a dozen people involved in the firm’s operations — is a window into challenges facing India’s startups. With limited domestic venture capital, firms like Byju’s have looked outward for support. That changed last year, when startup funding took a hit, falling to a four-year low by the first half of 2023.

Without easy access to global capital, companies are now facing greater scrutiny over corporate governance, jeopardizing India’s quest to pull even with the US and China as a tech capital of the world.

“If the situation is not contained quickly and guardrails are not put in place at Byju’s, it will affect India’s image as an investment destination among overseas funds,” said Jacob Mathew, a chairman of investment banking at Incred Capital Ltd.

Raveendran’s rise from a private tutor to the leader of a $22 billion company captivated global investors, including Sequoia Capital, Blackstone Inc. and Mark Zuckerberg’s foundation. During the pandemic, Raveendran cornered a majority of the ed-tech market in India.

But after classrooms reopened, concerns about Byju’s finances pricked at the firm’s reputation. Investors questioned why Raveendran delayed hiring a chief financial officer for years and acquired more than a dozen companies across the world at break-neck speed. Scores of employees have either left or been fired. Board members have resigned. And many teaching centers are nearly empty.

Raveendran’s supporters attribute missteps to the enthusiasm and naivete of an inexperienced founder who grew too quickly. Critics say he acted recklessly by withholding information about finances and failing to rigorously audit accounts. In India’s startup world, many see Byju’s as the highest-profile example of what happens when a business scales one of the fastest-growing economies during a boom — but fails to plan for a bust.

Raveendran and a spokesperson for Byju’s declined to comment.

Unusual Beginnings

Raveendran grew up in a village in the coastal state of Kerala and attended a local school where his father taught physics and his mother math. He was an unconventional student, according to people who knew him at the time, skipping classes to play football and preferring to teach himself at home.

After briefly working as an engineer, Raveendran began coaching students at a college in Bengaluru. Enrollment doubled every week, and Raveendran eventually moved classes into a sports stadium. Lessons were projected onto giant screens for thousands of students.

Raveendran’s teaching methods stood out in India, where good instructors are scarce and methodologies antiquated. He was adept at preparing students for fiercely competitive entrance exams to premier engineering and medical colleges.

Raveendran recruited his best students to teach alongside him and opened 41 coaching centers. In 2011, he registered Think and Learn Pvt Ltd. — the parent company of Byju’s. He co-founded the firm with Divya Gokulnath, a biotech engineer and former student whom he later married.

In 2015, Raveendran digitized his business, launching a self-learning app focused largely on math, science and English for primary school students.

“I’ve always enjoyed learning things on my own and also taught myself to hack exams, so it was easy to tutor others,” Raveendran said in a 2017 interview with Bloomberg News.

Surge in Cash

As tech spending surged during the late 2010s, investors lined up to support Raveendran.

Ranjan Pai, who runs one of the nation’s largest healthcare and education empires, said he agreed almost immediately to fund Byju’s. Raveendran capitalized on a spike in internet usage in India. Companies like Reliance Jio Infocomm Ltd. introduced data tariffs that ranked among the most affordable in the world.

“He stands out as one of the brightest entrepreneurs in the country — yet is a teacher at heart,” Pai said in a 2017 interview with Bloomberg.

Among Byju’s early backers was Sequoia Capital, which came aboard in 2015 and invested 4.8 billion rupees ($58 million), according to data from Tracxn. Soon after, Lightspeed Venture Partners and the Chan Zuckerberg Initiative — the Facebook founder’s philanthropic organization — participated in a $50 million funding round.

As capital flowed through the firm’s accounts, Raveendran acquired more than a dozen educational companies in India and abroad. When the pandemic pushed students online, the buyouts seemed prescient. Raveendran planned to take the company public through a SPAC merger. Some investors offered valuations as high as $48 billion, according to documents reviewed by Bloomberg.

Raveendran also tapped debt markets to fuel his acquisition spree. Though Byju’s sought to borrow only $500 million in 2021, overseas investors — including Blackstone Inc., Fidelity and GIC — put up enough cash to double the target size of the firm’s term loan B to $1.2 billion.

Cracks in the Edifice

But by the middle of 2022, problems began to compound. The SPAC boom petered out, along with demand for online tutoring. Employees questioned Raveendran’s business instincts: Even as the lifting of Covid restrictions battered ed-tech, he sought to raise more equity — rather than conserve cash and target profitability.

"chart")

That strategy hit a snag last July. Two key investors, Sumeru Ventures and Oxshott, failed to transfer about $250 million — part of the announced $800 million round — because of “macroeconomic reasons.” People familiar with the deal said Raveendran didn’t verify whether the investors had enough money before announcing the deal. (The funds never came through.)

Raveendran has avoided consulting investment bankers on deals, instead depending on Anita Kishore, his chief strategy officer, to execute most transactions, according to Byju’s employees.

Kishore and Raveendran declined to comment.

Meanwhile, Indian officials sent queries to Byju’s about why the firm couldn’t close its financial accounts for the fiscal year ending March 2021. India’s enforcement directorate, which investigates money laundering and forex violations, sent summons to company officials, people familiar with the matter said.

Charges weren’t filed against Byju’s after the raid in late April. But the Ministry of Corporate Affairs, India’s company regulator, will soon decide whether to open a formal probe, Bloomberg reported this month.

The MCA and enforcement directorate didn’t reply to requests for comment.

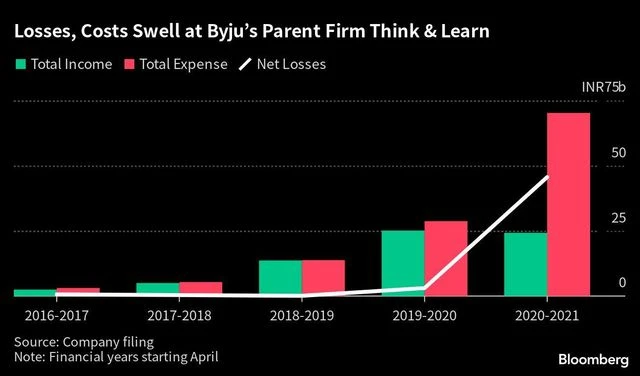

Eighteen months after the financial year’s close, Byju’s finally released audited statements. They showed losses of 45.7 billion rupees — a 13-fold jump from the previous year. Byju’s blamed the performance on accounting practices that deferred revenue to subsequent years. Others pointed out a massive increase in marketing spending.

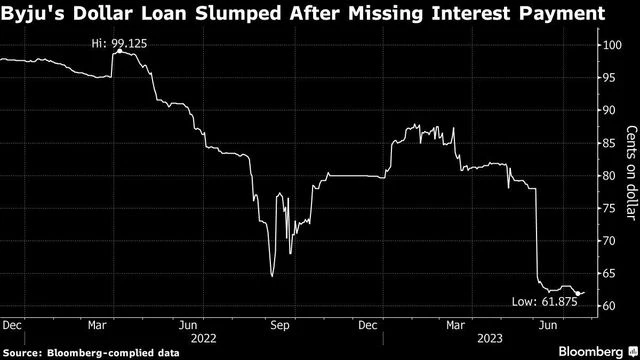

The firm’s finances alarmed investors. Some creditors, including Blackstone, offloaded their holdings, giving distressed investors in the US a chance to pick up the $1.2 billion loan at rates as low as 64 cents to a dollar.

Soon after buying the debt, those creditors began demanding accelerated payments as the firm had breached terms, including a September deadline for filing its results for the year ending March 31, 2022.

Following eight months of negotiations, Byju’s lenders in the US accused the firm in a Delaware lawsuit of hiding $500 million. They argued that Byju’s is in technical default over the $1.2 billion loan because the firm hasn’t provided regular financial updates.

"chart")

In June, Byju’s skipped a $40 million interest payment and filed its own lawsuit in New York, accusing the lenders of “bad-faith negotiating.” The company has argued the debt contract prohibits lenders from selling their stakes to certain investors, including those who specialize in distressed debt.

Shareholder Revolt

The stakes continue to rise. Representatives from three big investors — Peak XV, Prosus and the Chan Zuckerberg Initiative — recently quit Byju’s board. Deloitte Haskins & Sells also resigned as Byju’s auditor, citing the firm’s spotty financial records.

“Byju’s grew considerably since our first investment in 2018, but, over time, its reporting and governance structures did not evolve sufficiently for a company of that scale,” Prosus said in a July 25 statement, explaining why its director stepped down from Byju’s board.

In recent weeks, Raveendran and Ajay Goel — who joined Byju’s in April as its chief financial officer — hired an affiliate of accounting firm BDO to take over auditing. Goel has said that long-delayed financial accounts will be finalized by the end of September.

“The best of Byju’s is yet to come,” Raveendran told employees at a recent town hall, where he pushed back on criticisms. The company has “not come this far to only come this far.”

Raveendran is counting on a $1 billion equity investment from backers in the Middle East, which is expected as early as next month. He is also tapping some of his early backers in India to tide over the cash crunch.

If the funds come through, Byju’s could pay down creditors and buy out the revolting US-based investors, according to people following the negotiations, who didn’t want to be named because the discussions are private.

Meanwhile, earlier this week, lenders agreed to work toward restructuring the $1.2 billion loan by Aug. 3.

Most investors have slashed the firm’s valuation to less than $10 billion. But despite Byju’s rocky few months, many remain bullish, pointing to the firm’s strong assets, including 150 million customers.

“The company can still be brought back from the brink,” InCred’s Mathew said. “Some of its businesses have good cash flows, which can potentially attract value investors, who will come in with big cheques helping to sort out things.”

© 2023 Bloomberg L.P.

[ad_2]

Source link