[ad_1]

By Andy Mukherjee

Indian billionaire Anil Agarwal is shuffling the deck chairs, as his Vedanta Resources Ltd. approaches a $3 billion iceberg of dollar bonds due over the next two years. Can the commodities titan avoid the fate of the Titanic? The answer may only partly depend on investors’ greed for dividends.

Vedanta Ltd., the Indian publicly traded firm controlled by privately held Vedanta Resources, has announced a plan to split itself into six companies. For every share of Vedanta Ltd., investors will receive one share in each of the five new businesses: aluminum, oil and gas, power, steel and ferrous, and base metals. They will also retain their original share in Vedanta Ltd., which will continue to own 65% of Hindustan Zinc Ltd., apart from hosting new bets like semiconductors and LCD displays.

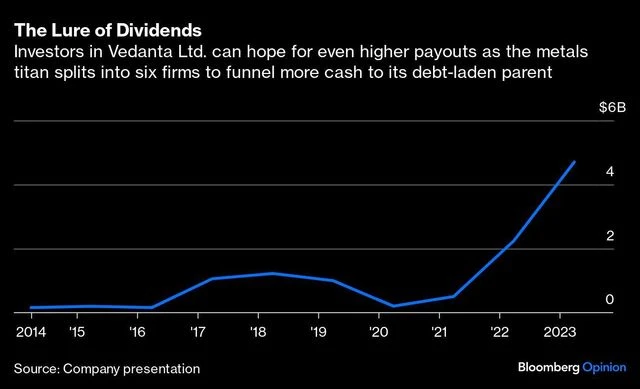

The carrot being dangled before minority investors is of payouts. A corporate presentation notes the “consistent shareholder returns” from more than $11 billion in dividends over the past decade. That was from one listed firm. Now there will be cash rolling in from half a dozen of them. Which is why perhaps the initial stock-market reaction to the spin-off had none of the pessimism that the news triggered in the bond market. Vedanta Ltd. shares rose nearly 4% on Tuesday, even as the Vedanta Resources dollar notes slipped deeper into distressed territory.

Equity investors are betting that the brood will funnel as much cash to the parent as possible. A part of it will come to them. Bondholders are saying it won’t be enough to make them whole, especially given UK-based Vedanta Resources’ large funding gap in the fiscal year that will start in April 2024. Both could be right.

Alternatively, Agarwal may be able to sell one or two of the operating companies, or extend the maturities on his debt. Slimming down may be a better route to staying afloat than asking bondholders to be patient. S&P Global Ratings cut its Vedanta Resources assessment to CCC from B- on the increased likelihood of a liability management exercise that “we could consider distressed under our criteria,” the agency said Friday. CCC is four rungs away from default, and according to S&P, there is a chance of further rating downside over the next three months.

Even if he isn’t out of options, the metals magnate is certainly in a pinch. Minus a boom in global commodities demand, saving the empire will be a touch-and-go affair. To get the benefit of the doubt from markets, Agarwal needs something more than dividends.

"chart")

The timeline of his troubles holds a clue as to what that may be.

The group’s debt woes intensified earlier this year. That was just when Gautam Adani, the businessman from Prime Minister Narendra Modi’s home state of Gujarat, came under a brutal short-seller attack, followed by intense scrutiny of his conglomerate’s corporate governance practices. Adani has denied all allegations. But more importantly, he has managed to keep his financing channels open, despite depressed equity and bond prices. He has persuaded lenders and investors that if India Inc. is a national team, he is its most valuable player. This is where Agarwal seems to be floundering. Forget being an MVP. Is he even on the team?

For one thing, his aggressive financial engineering has ended up annoying New Delhi. In January, the publicly traded part of Vedanta decided to offload some of its African zinc assets to Hindustan Zinc. That deal was valued at roughly $3 billion in phases over 18 months. Back then, Vedanta Ltd. was 70% owned by Vedanta Resources. The money floating up to the parent would have taken care of the latter’s liquidity needs. Except that the Indian government, which still owns about 30% of the privatized zinc miner, got spooked by the raid on its cash. A thwarted Agarwal had no option except to offload a small part of Vedanta Ltd. in the market.

The second thing that went wrong was semiconductors. India promised to pick up half the cost of chipmaking factories, and then balked at Agarwal when it looked like he couldn’t deliver on a 28-nanometer fab. In July, Hon Hai Technology Group, also known as Foxconn, pulled the plug on the $19 billion joint venture. The Taiwanese contract manufacturer may yet produce 40-nanometer microprocessors in partnership with STMicroelectronics NV. That leaves Agarwal, who once boasted of creating “a self-reliant Silicon Valley” in Modi’s Gujarat, in search of a new partner.

The tycoon can shuffle the financial deck chairs all he wants. But after this year’s misadventures, does he still have enough political clout to secure a lifeline? That’s what investors will need to know. And yes, they will want the dividends, too.

Disclaimer: This is a Bloomberg Opinion piece, and these are the personal opinions of the writer. They do not reflect the views of www.business-standard.com or the Business Standard newspaper

[ad_2]

Source link